HECM for Purchase Program

Enjoy your retirement on your terms.

Would you like to move to a house with modern amenities? Maybe you’d like to move closer to your children and grandchildren. Is your home too large now that the nest is empty? Whatever the reason, you might be wishing for a new home but didn’t think you could buy one.

In the past, your options were limited, but now there may be a way for you to achieve your dream of a new home: the Home Equity Conversion Mortgage for Purchase (H4P for short). The H4P lets seniors aged 62 and older purchase a home with approximately 50% down, helping you retain more of your financial nest egg.

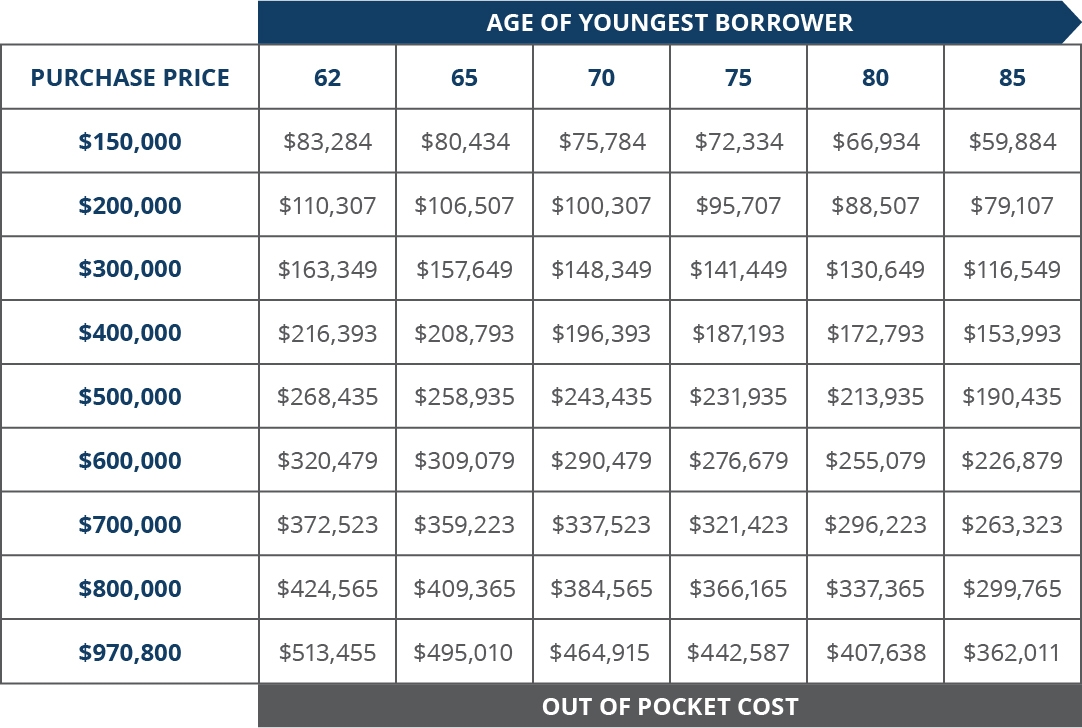

How much do you need for a down payment?

The matrix below demonstrates the increased home purchasing power gained by Americans (62-and-older) who use H4P.***

To use the matrix, match your age (on top of the chart) with the desired home purchase price (on the left side). The number where the age and purchase price intersect is the amount of down payment you will need at closing.

For example, a 65-year-old who wants to purchase a $300,000 home must provide a down payment of $157,649. The remainder of the balance ($142,351) is funded by a reverse mortgage loan.

*Must maintain the property as a primary residence and keep property taxes, insurance, and HOA dues current.

**In Texas all borrowers must be 62 or older.

*** This calculation is based on using HECM Fixed Rate of 3.56% as of January 18, 2022. Recent APRs range from 4.417- 5.502 APR. Loan charges will include origination fees, mortgage insurance premiums, and settlement costs which are to be determined. Most of these fees may be financed into the loan. Interest rates and funds available may change without notice and not be available at time of the loan commitment. Prices are subject to change. This information is for illustrative purposes only. Estimated closing cost, include up-front FHA mortgage insurance premium, range from $3000 – $19,416 depending upon the value of the home (included in mortgage). Closing costs vary from state to state and can affect out-of-pocket cost. Please check with your HECM Loan Officer for actual figures. Your loan balance and accrued interest will become due upon a maturity or default event such as no longer living in the home as your principal residence, failing to pay your hazard insurance or property taxes, or failing to maintain your property.

A better mortgage.

A better future.

We want to help you purchase your dream home using H4P. Contact us today or Find a Branch near you and together we can prepare you for your journey to financial security.

Potential Advantages

- Greater home purchasing power

- The ability to move into a home that better fits your needs

- Reduced out-of-pocket expenses since there is no monthly mortgage payment*

GET EDUCATED

Helping You to

Understand Your Options

Explore our free e-guides, vidtorials, and infographics on topics related to reverse mortgages.

Oct

20

2016

HECM / HOMEBUYING / REVERSE MORTGAGE

How HECM for Purchase (H4P) Can Help Retirees Buy a New Home

Mar

22

2018

HECM / HECM FOR PURCHASE / HOME EQUITY CONVERSION MORTGAGE / PURCHASE EXCEPTIONS

HECM For Purchase Exceptions to Remember

July

1

2021

HECM / RETIREMENT / REVERSE MORTGAGE

A HECM for Purchase Lets you Cash In by Moving Out

Things to know about Reverse Mortgages:

Things to know about Reverse Mortgages:

Things to know about Reverse Mortgages:

Things to know about Reverse Mortgages:- At the conclusion of a reverse mortgage, the borrower must repay the loan and may have to sell the home or repay the loan from other proceeds

- Charges will be assessed with the loan, including an origination fee, closing costs, mortgage insurance premiums and servicing fees

- The loan balance grows over time and interest is charged on the outstanding balance

- The borrower remains responsible for property taxes, hazard insurance and home maintenance, and failure to pay these amounts may result in the loss of the home

- Interest on a reverse mortgage is not tax-deductible until the borrower makes partial or full re-payment

More Resources

Open Mortgage offers a trove of resources from easy, quick videos to detailed educational resources. We’ve got you covered!

Search

Search